Budget Terms

The Province of Alberta legislates that municipalities must do annual market value-based assessments.

Who sets property values?

- Our third party contractor does property assessments

- Neither the Town nor the contractor controls factors that change the market value of your home, such as:

- Renovations

- Increases in market value

- If your assessed value goes up, your final tax amount will also go up even if the tax rates stay the same

Why is assessed value used for taxes?

- Property assessments help distribute the costs of services across residents and businesses

- The more expensive a property, the more tax is paid

- The assessed value is a property’s market value for July 1 of the previous year. It is the amount that a property might be expected to sell for on the open market

What do property assessment values fund?

Assessment value determines how much tax you pay on:

- Municipal tax

- Sylvan Lake Lodge Foundation tax

- Alberta Provincial Education tax

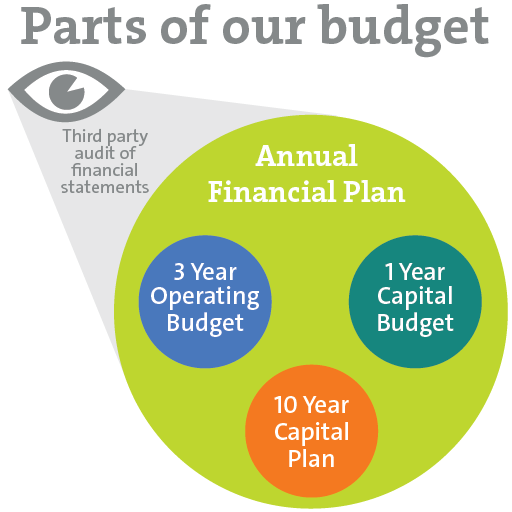

Every year we must create financial statements. Each year we must have an independent firm audit the statements. The financial statements must include a statement of:

- Financial position

- Operations

- Cash flows

- Changes in accumulated surplus

The Alberta Municipal Government Act requires us to complete this process.

- Identifies capital projects and how to fund them

- The capital budget is planned for separately from the operating budget

- The capital budget is based on capital funds, which are raised through tax dollars and other revenue

Capital projects are large and usually only happen once. They are part of the capital budget and can include projects like:

- 50 Avenue redevelopment

- Building new roads and maintaining existing roads

- Fleet costs such as replacing and buying pickup trucks or skid steers

- Replacing aging sewer and water mains

- Replacing playground equipment or campground furnishings, washrooms, and pathways

- Buying a new Protective Services generator or radio system

- Improving or renovating the NexSource Centre

The Alberta Municipal Government Act requires us to create a new capital budget every year.

Deliberate means "to think about or discuss issues and decisions carefully" (Merriam-Webster, n.d., Definition 1).

Staff and Council debate and discuss each department’s budget proposals. Budget debates happen in November – December each year. The process follows these steps:

- Each department presents their budget for the next year. They present new and existing expenses and ways to save money

- Council reviews and asks questions about each department’s budget

- Council may request changes and departments may make changes

- Council and departments consider public survey feedback. We collect feedback on engage.sylvanlake.ca

- We calculate the year's revenue requirement. This is how much money needed to cover all budgeted expenses

- Council approves:

- The residential and commercial property tax rates

- The draft operating budget and budget plan

- The final capital budget

- The 10-year capital plan

- Draft budget documents are placed online for public review

A draft budget is created after staff and Council deliberate (debate and discuss) the budget. The draft budget is presented to Lakers for review and feedback before it receives final approval. We collect feedback on engage.sylvanlake.ca

Draft budget public engagement options are the final opportunity for Lakers to give feedback on their next year's property taxes.

The Town of Sylvan Lake is a municipal government. There are three levels of government in Canada. Federal, provincial, and municipal. All municipalities must obey federal and provincial law. For example, the Town must follow the Municipal Government Act.

“Municipal governments are local elected authorities. They include cities, towns and villages, and rural (county) or metropolitan municipalities. They are created by the provinces and territories to provide services that are best managed under local control; from waste disposal and public transit to fire services, policing, community centres and libraries. A municipal government’s revenue is raised largely from property taxes and provincial grants.” (Plunkett, 2006)

“The Municipal Government Act (MGA) set the rules about how municipalities function, develop land, raise funds for things like services, and more” (Municipalities).

Our budget plans how we get every penny (revenue) and how we spend every penny (expenses). The budget makes sure we have money for essential services like snow removal. It also plans for capital projects like Pogadl Park. Council’s strategic priorities guide budget decisions. Administration (employees) create the budget. Council approves the budget.

The budget makes sure that today’s decisions meet our needs in the future. We review and adjust the budget every year. It includes:

- Operating budget for daily operating costs (3 year)

- Capital budget for capital projects

- Reserve projections

- Financial plan

The operating budget must estimate revenue, including:

- Taxation revenue

- User fees and charges (including Utilities)

- Government grants from other governments

- Franchise agreement revenue

- Licenses, permits, and rental income

- Development levies

- Fines and penalties

The Alberta Municipal Government Act requires us to create budgets and estimate revenues.

Operating budgets describe how we raise the money to pay for the daily expenses to keep services running for one year, such as:

- Staff wages and benefits

- Contracted services

- Policing and bylaw services

- Goods and supplies

- Utilities and fuels

- Debt repayment

The operating budget is planned for separately from the capital budget.

Revenue pays for our public services. It pays for everything from clean water and snow removal to playgrounds. The Town’s revenue comes from a variety of sources, such as:

- Collected through property taxes:

- Residential property taxes

- Commercial property taxes

- A recreation levy pays the debt for building the NexSource Centre

- A transportation levy pays for roads

- You may notice education and seniors' fees on property taxes. The Town collects these on behalf of the Province and Lodge. They do not add to the Town’s revenue

- Other sources such as transfer from reserves, fines, NexSource food and beverage sales, return on investments, special event revenue

- Atco and Fortis fees (franchise contracts)

- Government grants such as federal and provincial funding

- Rentals and Other income such as park picnic shelters rentals

- Goods and services like waste transfer site fees, parking fees, and food and beverage sales at the NexSource Centre

- Licenses and fees from business licenses, development fees, and NexSource memberships

- Utility bill revenue, which pays for water, sewer, wastewater infrastructure. Utility services are self-funded through utility bill revenue, not property taxes

This plan identifies future capital projects. It describes how we fund those projects.

10-year capital plans are required by the Alberta Municipal Government Act.

To finance large-scale projects, the town gradually sets aside a small amounts of revenue over many years to pay for major infrastructure projects.

"This approach minimizes the use of financing, which allows municipalities to stay within debt limits and ultimately saves municipal taxpayers money by reducing interest costs. In a municipal context, funds set aside for such projects are known as 'reserves.'

Put simply, financial reserves are a means to pay for the construction or purchase of assets in the future, and to fund asset depreciation to ensure aging infrastructure can be maintained to continue providing necessary levels of service." (Rural Municipalities of Alberta, 2019)

-

Merriam-Webster. (n.d.). Deliberate. In Merriam-Webster.com dictionary. Retrieved October 16, 2023, from https://www.merriam-webster.com/dictionary/deliberate

-

Municipalities. Government of Alberta About municipalities. Retrieved from: https://www.alberta.ca/about-municipalities.aspx

-

Plunkett, T.J. (2006). In The Canadian Encyclopedia Online. Retrieved from: https://www.thecanadianencyclopedia.ca/en/article/municipal-government

- Rural Municipalities of Alberta. (2019) Understanding Municipal Financial Reserves. Retrieved from: https://rmalberta.com/wp-content/uploads/2019/11/RMA-Municipal-Financial-Reserve-Report.pdf